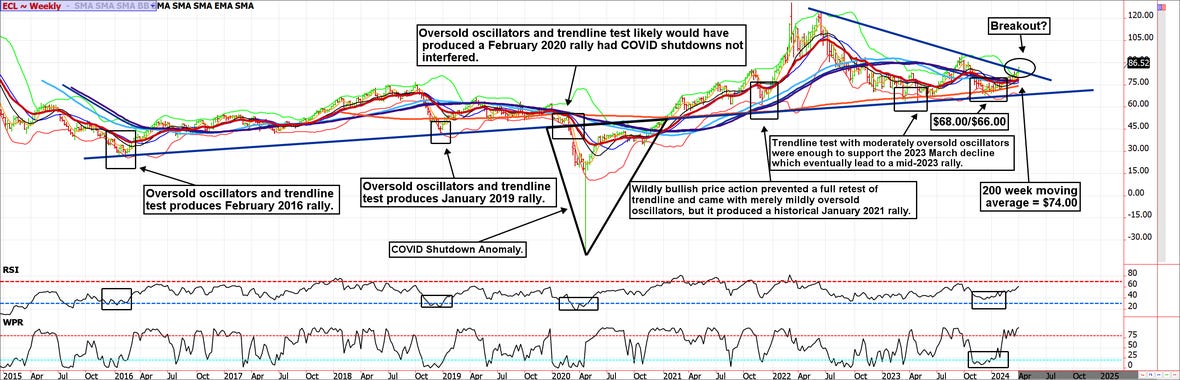

Crude oil has Rallied without the Help of Speculators or Chinese Demand

The oil market has quietly assembled an impressive $15.00 per barrel rally. The lack of fanfare can likely be attributed to the lack of volatility.

Crude oil has Rallied without the Help of Speculators or Chinese Demand

The oil market has quietly assembled an impressive $15.00 per barrel rally. The lack of fanfare can likely be attributed to the lack of volatility. There were days in 2022 when oil jumped or collapsed from $10.00 to $15.00 in a single trading session, yet the run from $70.00 to $85.00 took about three months. These slow grinding rallies are generally not to be sold into (been there and done that, don't do it).

The slow and steady price increase has occurred without much help from speculators. According to the COT Report (Commitments of Traders) issued by the CFTC (Commodity Futures Trading Commission), large speculators (known as the smart money) are holding a net long position of about 250,000; this pales in comparison to the all-time-high position of over 700,000. Our takeaway from this data is that plenty of sidelined speculator money might start getting FOMO (fear of missing out) should the breakout above $84.00 hold on a weekly basis (Friday's close). I spoke about this on the Cow Guy Close television program aired on RFD-TV.

The US is producing and exporting more crude oil now than ever before; as a result, they have picked up more market share and put some pressure on OPEC to tap the brakes on their production cuts. However, as of the last meeting, OPEC has made it clear they have worked too hard to manipulate prices higher to give up now. The cartel affirmed their pledged production cuts and scolded members for cheating (the reductions have been larger on paper than in reality due to some members producing beyond their quotas). Thus, OPEC supply cuts and Russian supply disruptions due to the war offset some of the domestic production overachievements.

We can't talk about oil prices, and OPEC's manipulation of those prices, without mentioning the US policy of draining the SPR (Strategic Petroleum Reserve). The US successfully pressured oil prices by releasing stockpiles from the reserve. Just as the OPEC production cuts are effective but obviously temporary, so was the SPR release program. However, the US will not have the same tool at its disposal in the future. In early 2022, the SPR held about six hundred million barrels, it is currently at about 363 million. This isn't as significant as it appears. The daily global demand for crude oil is about 100 million barrels, so a drawdown from the SPR of 240 million barrels is about two and a half days of usage. The SPR sales weren't necessarily a game changer for the supply/demand fundamentals, but they successfully thwarted exuberant speculation on higher oil prices and calmed the climate; timing is everything.

According to the US government, the average SPR release sale price was $95.00 per barrel, and they are targeting refilling barrels at $79.00 or lower. Due to prices drifting above their desired repurchase price, the administration has announced that they will cancel SPR refill operations for now. However, the information available to me suggests they were merely targeting 3 million barrels a month in refill purchases. This snail's pace doesn't seem to give the oil market the respect it deserves based on historical volatility. At that pace, if they made a monthly purchase in that quantity, it would take 79 months or 6.5 years to get back to the starting point of six hundred million barrels. The commodity markets are not predictable in the short-term, but long-term price projections are nothing more than an academic science, and such analysis is almost never accurate. When oil was nearly free in the spring of 2020, precisely zero price models were calling for the price to be near $130.00 two years later, but that happened. With this in mind, and assuming the reported average sell price of $95.00, refilling the SPR for $85.00 per barrel isn't bad. In fact, it would be a great trade for taxpayers. We will almost certainly see oil prices below $79.00 at some point in the next six and a half years, but the risk of not having the opportunity cost of not refilling the SPR at reasonable prices is national security.

Nevertheless, tight supplies are vulnerable to being exposed by the continuation of OPEC production cuts, the need for the US to refill the SPR, and Chinese demand showing signs of life. If the breakout holds, as expected, we continue to believe $100.00 oil is in play.

*There is substantial risk of loss in trading futures and options. There are no guarantees in speculation; most people lose money trading commodities. Past performance is not indicative of future results.

Seasonality is already factored into current prices, any references to such does not indicate future market action.

** These recommendations are a solicitation for entering into derivatives transactions. All known news and events have already been factored into the price of the underlying derivatives discussed. From time to time persons affiliated with Zaner, or its associated companies, may have positions in recommended and other derivatives. Past performance is not indicative of future results. The information and data in this report were obtained from sources considered reliable. Their accuracy or completeness is not guaranteed. Any decision to purchase or sell as a result of the opinions expressed in this report will be the full responsibility of the person authorizing such transaction. Seasonal tendencies are a composite of some of the more consistent commodity futures seasonals that have occurred over the past 15 or more years. There are usually underlying, fundamental circumstances that occur annually that tend to cause the futures markets to react in similar directional manner during a certain calendar year. While seasonal trends may potentially impact supply and demand in certain commodities, seasonal aspects of supply and demand have been factored into futures & options market pricing. Even if a seasonal tendency occurs in the future, it may not result in a profitable transaction as fees and the timing of the entry and liquidation may impact on the results. No representation is being made that any account has in the past, or will in the future, achieve profits using these recommendations. No representation is being made that price patterns will recur in the future.